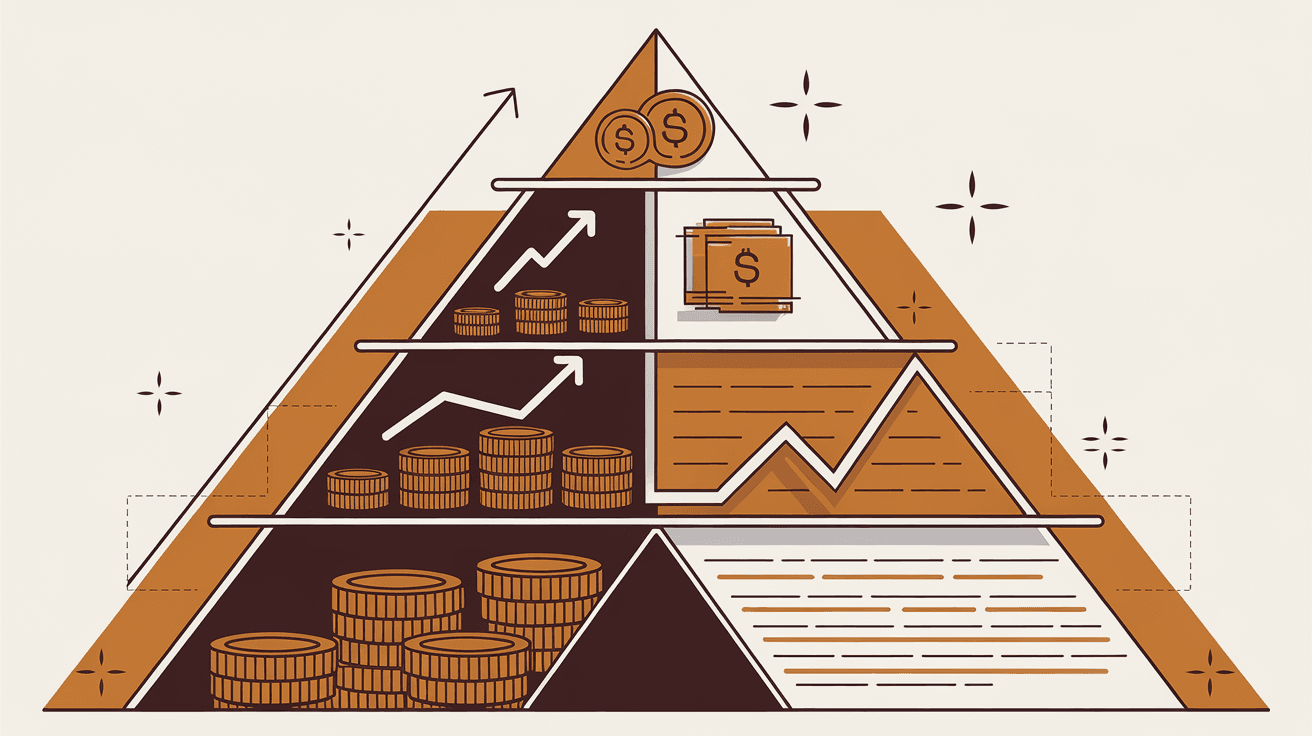

The Wealth Building Hierarchy: What to Optimize First

The 5-Level Framework for Smart Financial Prioritization

Most people obsess over finding the perfect stock while paying 23% credit card interest—like optimizing your car's aerodynamics with the parking brake on.

People waste enormous energy on complex financial strategies while ignoring basic inefficiencies that cost them thousands. Without a clear priority framework, they optimize the wrong things in the wrong order, sabotaging their wealth-building potential.

The Wealth Building Hierarchy: What to Optimize First

The average American spends 23 hours researching their next phone purchase but less than 3 hours annually reviewing their financial priorities. This backwards approach explains why 64% of Americans can't handle a $400 emergency despite having investment accounts.

The Wealth Building Hierarchy solves this by creating a clear optimization sequence. Like Maslow's hierarchy of needs, each level must be secured before moving to the next. Skip steps, and your financial foundation crumbles.

The Framework Name: The Wealth Building Hierarchy

This five-level pyramid prioritizes financial decisions by impact and urgency. Each level represents a prerequisite for the next, ensuring you build wealth on solid ground rather than financial quicksand.

Why It Works

The hierarchy works because of three psychological and mathematical principles:

Mathematical Certainty vs. Probability: Lower levels offer guaranteed returns (paying off 18% credit card debt = guaranteed 18% return). Higher levels involve probability (stock market averages 10% but varies wildly).

Behavioral Momentum: Small, certain wins at the base create confidence and habits needed for complex decisions at the top.

Risk Mitigation: Each level reduces specific risks before taking on new ones. You can't afford investment volatility without an emergency buffer.

Research by MIT's Behavioral Economics Lab shows people who follow hierarchical financial frameworks accumulate 34% more wealth over 10 years than those who don't, primarily because they avoid costly mistakes rather than finding better investments.

The Components

Level 1: Stop the Bleeding (Guaranteed High Returns)

Target: Eliminate high-interest debt and obvious inefficiencies Priority: Any debt above 7% interest rateThis level offers the highest guaranteed returns you'll ever see. Paying off a 19% credit card is equivalent to earning 19% risk-free—better than Warren Buffett's average.

Actions:

- List all debts by interest rate

- Pay minimums on everything, attack highest rate first

- Audit recurring subscriptions (average household wastes $273/month)

- Switch to high-yield savings (currently 4-5% vs. 0.01% at big banks)

Level 2: Build Your Foundation (Liquidity and Protection)

Target: 3-6 months expenses in emergency fund + basic insurance Priority: Liquidity before investmentsThis level protects against life's inevitable surprises. Without it, you'll be forced to sell investments at the worst times or go into debt.

Emergency Fund Sizing:

- W-2 employees: 3-4 months expenses

- Commission/freelance: 6-8 months expenses

- Business owners: 8-12 months expenses

Research insight: Households with emergency funds are 70% less likely to miss investment contributions during market downturns (Vanguard, 2021).

Level 3: Capture Free Money (Employer Matching and Tax Advantages)

Target: Maximize employer 401k match + optimize tax-advantaged accounts Priority: Free money before optimizing returnsThis is the closest thing to free money in finance. Not capturing employer matching is leaving guaranteed 50-100% returns on the table.

Sequence:

HSA advantage: The only account with triple tax benefits—deductible contributions, tax-free growth, tax-free withdrawals for medical expenses. After age 65, functions like traditional IRA.

Roth vs. Traditional decision: If you expect higher tax rates in retirement (early career, growing income), choose Roth. If you expect lower rates (peak earners nearing retirement), choose Traditional.

Level 4: Systematic Wealth Building (Index Fund Investing)

Target: Consistent, diversified investing in low-cost index funds Priority: Time in market over timing the marketWith your foundation secure and free money captured, focus on systematic wealth building through broad market exposure.

The 3-Fund Portfolio (recommended by Bogleheads):

- 60-80% Total Stock Market Index

- 10-20% International Stock Index

- 10-20% Bond Index

- 20s-30s: 90% stocks, 10% bonds

- 40s: 80% stocks, 20% bonds

- 50s: 70% stocks, 30% bonds

- 60s+: 60% stocks, 40% bonds

Cost matters: A 1% annual fee costs you $590,000 over 40 years on a $500,000 portfolio (assuming 7% returns). Choose funds with expense ratios under 0.1%.

Level 5: Advanced Optimization (Alternative Investments and Tax Strategies)

Target: Real estate, individual stocks, tax optimization, business ownership Priority: Only after mastering the basicsThis level is for surplus capital after maxing out tax-advantaged accounts and building a solid index fund base.

Real Estate Investment:

- Primary residence: Buy when you can afford 20% down + 6 months of payments saved

- Rental property: Only if you can handle being a landlord or afford property management

- REITs: Easier real estate exposure through index funds

Advanced Tax Strategies:

- Tax-loss harvesting in taxable accounts

- Asset location optimization (bonds in tax-advantaged accounts)

- Backdoor Roth conversions for high earners

- Mega backdoor Roth if plan allows

Application Guide

Step 1: Calculate Your Current Level Complete Level 1 before moving to Level 2. No exceptions.

Step 2: Set Level-Specific Goals

- Level 1: Target debt payoff date

- Level 2: Emergency fund target amount

- Level 3: Maximum employer match capture date

- Level 4: Monthly investment automation amount

- Level 5: Surplus capital allocation plan

- Review progress on current level

- Adjust if life circumstances change

- Resist jumping levels prematurely

- Automatic debt payments

- Automatic emergency fund contributions

- Automatic investment contributions

- Automatic rebalancing

Example Application

Sarah, 28, Marketing Manager, $75k salary:

Current state: $8k credit card debt (22% interest), $2k savings, contributing 3% to 401k (employer matches 6%), no other investments.

Level 1 (6 months):

- Stop 401k contributions temporarily

- Pay $1,500/month toward credit card

- Cancel unused subscriptions ($180/month savings)

- Switch to high-yield savings

- Build $15k emergency fund ($1,250/month)

- Get term life insurance ($30/month)

- Restart 401k at 6% for full match

- Open and max Roth IRA ($542/month)

- Increase 401k contribution 1% annually

- Invest additional surplus in taxable account

- Use 3-fund portfolio approach

- Consider house purchase

- Explore backdoor Roth strategies as income grows

Common Mistakes

Mistake 1: Level Jumping Investing in crypto while carrying credit card debt. The guaranteed 20% "return" from debt payoff beats any speculative investment.

Mistake 2: Analysis Paralysis at Higher Levels Spending months researching the perfect investment allocation while not maximizing employer match. Perfect is the enemy of good.

Mistake 3: Ignoring Insurance Building wealth without protection. One medical emergency can wipe out years of careful investing.

Mistake 4: Lifestyle Inflation Increasing spending as income grows instead of moving up the hierarchy faster. Each raise should accelerate your level progression.

Mistake 5: Emotional Decisions Abandoning the hierarchy during market volatility. The framework exists precisely for these moments—trust the process.

The Wealth Building Hierarchy isn't sexy, but it works. It's the difference between random financial activity and systematic wealth building. Master the boring basics, and the exciting stuff becomes possible.

Key Takeaways

- 1.Guaranteed returns (debt payoff) always beat speculative investments

- 2.Each level must be completed before advancing to the next

- 3.Automation prevents emotional decision-making that destroys wealth

- 4.The hierarchy protects you from optimizing the wrong things at the wrong time

Your Primary Action

List all your debts by interest rate and calculate exactly how much you're paying in interest monthly—this number will motivate you to complete Level 1 immediately.

Expected time to results: 2-4 weeks to reorganize priorities, 6-18 months to complete foundation levels

Free Wealth Tools

Action Steps

- 1List all debts by interest rate and minimum payments to identify highest-priority payoffs

- 2Calculate your current emergency fund coverage and set a 3-6 month expense target

- 3Review all high-interest debt (above 7%) and create an aggressive payoff timeline

- 4Audit current investment allocations and pause contributions until lower hierarchy levels are complete

- 5Set up automatic transfers to systematically work through each hierarchy level

How to Know It's Working

- High-interest debt balance decreasing by specific dollar amounts monthly

- Emergency fund reaching 3-6 months of expenses within target timeframe

- Net worth increasing consistently as debt decreases and savings grow

Need this built for your business?

I build AI systems, automation workflows, and custom tools that turn these strategies into running infrastructure. Chemical engineer turned AI architect — I speak both the theory and the implementation.

Related Articles

Did you find this article helpful?

Comments

The Weekly Decode

One insight per dimension, every week. What they're hiding about your food, your money, your mind, your relationships, and your sense of meaning — backed by research, delivered free. No sponsors. No affiliates. No bullshit.

Ready to take action?

Get personalized insights and track your progress across all five dimensions with The Mirror.

Access The Mirror